ASC 842 cash flow statement examples & lease accounting

ASC 842 is the lease accounting standard introduced by the Financial Accounting Standards Board (FASB). It replaces ASC 840 and introduces sweeping changes to how organizations report leases. One of the biggest changes is how leases appear on financial statements, particularly the statement of cash flows.

Under ASC 840, most operating leases were treated as off-balance-sheet items. A company could have hundreds of millions of dollars in lease obligations, yet these would only appear in the footnotes to the financial statements. Investors and analysts had to work harder to understand the true financial position of the business, and comparing companies was often difficult.

ASC 842 solves this problem by requiring nearly all leases to be recognized on the balance sheet. This means businesses must now record a right-of-use (ROU) asset and a corresponding lease liability for both operating and finance leases. The change ensures that stakeholders can clearly see lease commitments, but it also directly affects the ASC 842 cash flow statement.

Here’s what it means in practice:

Operating leases: Payments are recorded in operating activities, as before, but with a corresponding liability and asset shown on the balance sheet.

Finance leases: Principal payments are shown in financing activities, while interest payments are shown in operating activities.

This classification improves transparency but also affects key performance metrics. Operating cash flow can look higher or lower depending on how leases are structured. Debt ratios also shift because lease liabilities are now counted as debt-like obligations.

For example, imagine a retail chain with 200 store leases. Under ASC 840, most of these leases would be hidden off the balance sheet. Under ASC 842, the company must now report them as liabilities and reflect payments in the cash flow statement. Analysts and lenders can more easily see the company’s obligations, and management must explain how lease cash flows affect liquidity.

The impact on cash flow reporting is therefore more than just a technical accounting change. It reshapes how companies present themselves to investors, how analysts value businesses, and how lenders assess credit risk.

ASC 842 cash flow statement example and presentation

A practical ASC 842 cash flow statement example makes the new presentation clear. The standard requires companies to classify lease payments differently based on whether they are operating or finance leases.

Finance leases under ASC 842

Finance leases (previously known as capital leases) are treated similarly to debt. Payments must be split between principal and interest:

Principal portion → financing activities

Interest portion → operating activities

This separation highlights both the repayment of the liability and the cost of financing.

Operating leases under ASC 842

Operating leases remain within operating activities. However, under ASC 842 they are no longer “invisible.” The related ROU asset and lease liability appear on the balance sheet, so stakeholders see both the ongoing cash payments and the balance sheet impact.

Example statement of cash flows presentation

Here is a simplified ASC 842 statement of cash flows example:

Activity | Classification | Example amount |

|---|---|---|

Principal payment (finance lease | Financing | $50,000 |

Interest payment (finance lease) | Operating | $10,000 |

Lease payment (operating lease) | Operating | $30,000 |

This shows how $90,000 in total lease payments is split across two categories. If the company had only operating leases, the full $90,000 would appear in operating activities. If it had only finance leases, $50,000 would be in financing and $10,000 in operating.

Why presentation matters

Companies often confuse ASC 842 balance sheet presentation with cash flow presentation ASC 842. While both deal with leases, they answer different questions:

The balance sheet presentation shows the total obligations and assets tied to leases.

The cash flow presentation shows how payments actually affect cash movement in a period.

Auditors pay close attention to these classifications. Misclassifying principal payments as operating activities or failing to split interest correctly can result in audit findings and compliance issues. For this reason, many organizations prepare ASC 842 cash flow presentation examples as internal guidance and use specialized software to avoid mistakes.

How SOFT4Lessee streamlines ASC 842 compliance and reporting

Complying with ASC 842 manually can be daunting. A company with dozens of leases must calculate lease liabilities, track right-of-use assets, split lease payments correctly, and update disclosures each reporting period. For businesses with hundreds or thousands of leases, this quickly becomes unmanageable without automation.

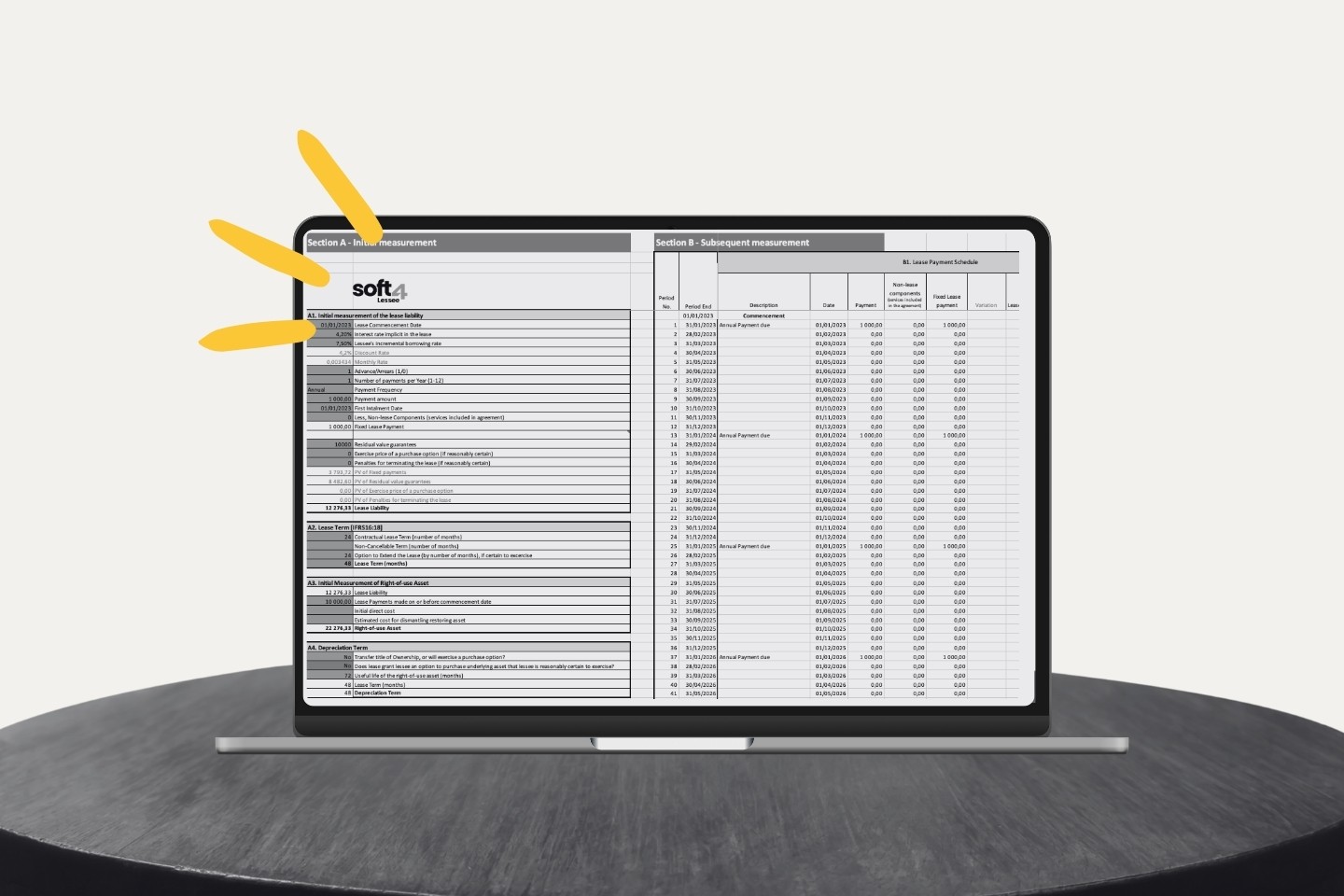

This is where SOFT4Lessee provides value. It is lease accounting software designed to automate ASC 842, IFRS 16, and AASB 16 compliance. Instead of relying on spreadsheets, companies can centralize lease data and generate audit-ready reports.

How SOFT4Lessee helps

Automated calculations: SOFT4Lessee automatically calculates lease liabilities and right-of-use assets. It splits finance lease payments into principal and interest so that the ASC 842 cash flow statement presentation is always accurate.

Pre-built reporting templates: Finance teams can generate cash flow statements, balance sheets, and disclosures with one click. These reports are built to align with ASC 842, reducing the chance of errors.

ERP integration: The software connects with Microsoft Dynamics 365 Business Central and other ERP systems. Lease data flows into the general ledger, ensuring consistent ASC 842 financial statement presentation.

Audit-ready trail: Every lease and calculation is tracked, giving auditors a clear line of sight into how numbers were derived.

Support for multiple standards: Multinational companies often need to comply with ASC 842, IFRS 16, and AASB 16 simultaneously. SOFT4Lessee allows parallel reporting under all three standards.

Real-world scenario

Consider a logistics company with 500 vehicle leases. Each lease must be tracked, updated for modifications, and reported under ASC 842. Without automation, the accounting team would spend weeks preparing disclosures. With SOFT4Lessee, they import all contracts, let the system calculate liabilities and ROU assets, and generate a complete ASC 842 statement of cash flows example in minutes.

Ongoing compliance support

ASC 842 compliance is not a one-time task. Leases change frequently — they may be renewed, extended, or terminated early. SOFT4Lessee makes ongoing compliance easier by:

Automatically adjusting schedules for modifications

Keeping all lease contracts in one central repository

Providing built-in disclosure templates that are always audit-ready

By automating compliance and reporting, SOFT4Lessee reduces risk, saves time, and ensures accuracy in every reporting cycle.

Frequently asked questions about ASC 842 cash flow presentation

How are lease payments presented on the cash flow statement under ASC 842?

Finance lease principal payments are deposited into financing activities, while finance lease interest payments and operating lease payments are presented in operating activities.

What is the difference between operating and finance lease cash flow classification?

Operating leases are straightforward - the entire payment goes to operating activities. Finance leases require a split between principal (financing) and interest (operating).

What are the key disclosure requirements for ASC 842 cash flows?

Organizations must disclose total cash paid for leases, broken down by classification. This ensures transparency about lease-related outflows.

How does SOFT4Lessee support ASC 842 cash flow reporting?

It automates the classification, generates compliance-ready reports, and creates audit trails for every calculation.

Can SOFT4Lessee handle ASC 842, IFRS 16, and AASB 16?

Yes. It is designed to generate parallel reports for multiple accounting standards, which is essential for multinational organizations.

Comparing ASC 842, IFRS 16, and AASB 16 cash flow requirements

Lease accounting is not uniform across the world. While the United States follows ASC 842, many international businesses must also comply with IFRS 16 (International Financial Reporting Standards) or AASB 16 (Australian Accounting Standards Board). At first glance, these standards look similar, all aim to bring leases onto the balance sheet, but they differ in how lease payments are treated in the statement of cash flows. Understanding these differences is critical for multinational companies, as the same lease may appear differently depending on the standard applied.

ASC 842 (US GAAP)

ASC 842 is designed to improve transparency without completely overhauling the treatment of operating leases in the cash flow statement.

Finance leases:

Principal portion → classified as financing activity

Interest portion → classified as operating activity

Operating leases:

Entire lease payment → classified as operating activity

This approach creates a distinction between finance and operating leases. It preserves comparability with historic US GAAP reporting while still recognizing lease obligations on the balance sheet.

IFRS 16 (International)

IFRS 16 takes a different approach, aiming for a single model of lease accounting. Under IFRS 16, almost all leases are treated similarly to finance leases under ASC 842.

Lease liability payments:

Principal portion → classified as financing activity

Interest portion → classified as either financing activity or operating activity, depending on accounting policy choice

This means that under IFRS 16, operating leases no longer appear fully in operating cash flows. Instead, much of the lease payment shifts to financing activities, which can make operating cash flow look stronger compared to ASC 842.

For example, a company with large property leases may report lower operating cash outflows under IFRS 16 than it would under ASC 842. This difference can affect key ratios such as operating cash flow coverage and free cash flow, making cross-border comparisons tricky.

AASB 16 (Australia)

AASB 16 is Australia’s equivalent of IFRS 16, adopted by the Australian Accounting Standards Board. In practice, it mirrors IFRS 16, with only minor adjustments for local reporting rules.

Lease liability payments:

Principal portion → classified as financing activity

Interest portion → classified as either financing or operating, based on policy choice

Operating leases:

Like IFRS 16, treated in the same way as finance leases, removing the operating lease category from cash flow classification

For Australian companies, the main difference lies in additional disclosure requirements specific to AASB. However, in terms of cash flow presentation, AASB 16 aligns with IFRS 16.

Best practices for lease data preparation and transition to ASC 842

Transitioning from ASC 840 to ASC 842 requires more than just learning new rules. Success depends on preparing accurate, complete lease data. Poor-quality data is one of the biggest challenges organizations face.

Best practices include:

Collect all lease contracts: Many businesses underestimate their lease portfolios. Be thorough — include real estate, vehicles, and even office equipment.

Abstract key terms: Capture start dates, end dates, payment schedules, renewal options, and escalation clauses.

Clean data: Resolve inconsistencies, remove duplicates, and ensure contracts are complete.

Use software tools: Automate calculations and reporting with systems like SOFT4Lessee to avoid manual errors.

Maintain documentation: Keep audit trails for all contracts and adjustments.

Organizations can reduce risk and ensure a smooth transition to ASC 842 by following these steps.

Get started with SOFT4Lessee for ASC 842 lease accounting

Managing leases under ASC 842 doesn’t need to be overwhelming. SOFT4Lessee helps organizations of all sizes comply with the standard efficiently.

For example, a mid-sized company with 200 leases once spent weeks preparing disclosures. After adopting SOFT4Lessee, it could produce an accurate ASC 842 cash flow statement presentation in hours. Audits became smoother, and management gained more confidence in the numbers.

The software scales for small and large portfolios. Smaller firms can start with an Excel-based calculator, while larger organizations can use enterprise licenses that handle thousands of leases. Each client receives training resources and a dedicated partner manager for support.

By adopting SOFT4Lessee, companies gain accurate reporting, faster close cycles, and reduced compliance risk.

Ensuring accurate ASC 842 cash flow reporting with automation

ASC 842 has transformed how leases are reported. Companies must now recognize right-of-use assets and lease liabilities and carefully classify payments in the statement of cash flows. While this improves transparency, it also adds complexity.

Using an ASC 842 cash flow statement example helps illustrate the changes, but software like SOFT4Lessee makes compliance manageable. SOFT4Lessee helps organizations stay compliant and reduce the burden of lease accounting by automating calculations, supporting multiple standards, and providing audit-ready reports.

For companies preparing for the next reporting cycle, investing in automation is no longer optional - it’s a practical step toward accuracy, efficiency, and long-term compliance.

Related articles

ASC 842 cash flow statement examples & lease accounting

ASC 842 is the lease accounting standard introduced by the Financial Accounting Standards Board (FASB). It replaces ASC 840 and introduces sweeping changes to how organizations report leases. One of the biggest changes is how leases appear on financial statements, particularly the statement of cash flows.

Under ASC 840, most operating leases were treated as off-balance-sheet items. A company could have hundreds of millions of dollars in lease obligations, yet these would only appear in the footnotes to the financial statements. Investors and analysts had to work harder to understand the true financial position of the business, and comparing companies was often difficult.

ASC 842 solves this problem by requiring nearly all leases to be recognized on the balance sheet. This means businesses must now record a right-of-use (ROU) asset and a corresponding lease liability for both operating and finance leases. The change ensures that stakeholders can clearly see lease commitments, but it also directly affects the ASC 842 cash flow statement.

Here’s what it means in practice:

Operating leases: Payments are recorded in operating activities, as before, but with a corresponding liability and asset shown on the balance sheet.

Finance leases: Principal payments are shown in financing activities, while interest payments are shown in operating activities.

This classification improves transparency but also affects key performance metrics. Operating cash flow can look higher or lower depending on how leases are structured. Debt ratios also shift because lease liabilities are now counted as debt-like obligations.

For example, imagine a retail chain with 200 store leases. Under ASC 840, most of these leases would be hidden off the balance sheet. Under ASC 842, the company must now report them as liabilities and reflect payments in the cash flow statement. Analysts and lenders can more easily see the company’s obligations, and management must explain how lease cash flows affect liquidity.

The impact on cash flow reporting is therefore more than just a technical accounting change. It reshapes how companies present themselves to investors, how analysts value businesses, and how lenders assess credit risk.

ASC 842 cash flow statement example and presentation

A practical ASC 842 cash flow statement example makes the new presentation clear. The standard requires companies to classify lease payments differently based on whether they are operating or finance leases.

Finance leases under ASC 842

Finance leases (previously known as capital leases) are treated similarly to debt. Payments must be split between principal and interest:

Principal portion → financing activities

Interest portion → operating activities

This separation highlights both the repayment of the liability and the cost of financing.

Operating leases under ASC 842

Operating leases remain within operating activities. However, under ASC 842 they are no longer “invisible.” The related ROU asset and lease liability appear on the balance sheet, so stakeholders see both the ongoing cash payments and the balance sheet impact.

Example statement of cash flows presentation

Here is a simplified ASC 842 statement of cash flows example:

Activity | Classification | Example amount |

|---|---|---|

Principal payment (finance lease | Financing | $50,000 |

Interest payment (finance lease) | Operating | $10,000 |

Lease payment (operating lease) | Operating | $30,000 |

This shows how $90,000 in total lease payments is split across two categories. If the company had only operating leases, the full $90,000 would appear in operating activities. If it had only finance leases, $50,000 would be in financing and $10,000 in operating.

Why presentation matters

Companies often confuse ASC 842 balance sheet presentation with cash flow presentation ASC 842. While both deal with leases, they answer different questions:

The balance sheet presentation shows the total obligations and assets tied to leases.

The cash flow presentation shows how payments actually affect cash movement in a period.

Auditors pay close attention to these classifications. Misclassifying principal payments as operating activities or failing to split interest correctly can result in audit findings and compliance issues. For this reason, many organizations prepare ASC 842 cash flow presentation examples as internal guidance and use specialized software to avoid mistakes.

How SOFT4Lessee streamlines ASC 842 compliance and reporting

Complying with ASC 842 manually can be daunting. A company with dozens of leases must calculate lease liabilities, track right-of-use assets, split lease payments correctly, and update disclosures each reporting period. For businesses with hundreds or thousands of leases, this quickly becomes unmanageable without automation.

This is where SOFT4Lessee provides value. It is lease accounting software designed to automate ASC 842, IFRS 16, and AASB 16 compliance. Instead of relying on spreadsheets, companies can centralize lease data and generate audit-ready reports.

How SOFT4Lessee helps

Automated calculations: SOFT4Lessee automatically calculates lease liabilities and right-of-use assets. It splits finance lease payments into principal and interest so that the ASC 842 cash flow statement presentation is always accurate.

Pre-built reporting templates: Finance teams can generate cash flow statements, balance sheets, and disclosures with one click. These reports are built to align with ASC 842, reducing the chance of errors.

ERP integration: The software connects with Microsoft Dynamics 365 Business Central and other ERP systems. Lease data flows into the general ledger, ensuring consistent ASC 842 financial statement presentation.

Audit-ready trail: Every lease and calculation is tracked, giving auditors a clear line of sight into how numbers were derived.

Support for multiple standards: Multinational companies often need to comply with ASC 842, IFRS 16, and AASB 16 simultaneously. SOFT4Lessee allows parallel reporting under all three standards.

Real-world scenario

Consider a logistics company with 500 vehicle leases. Each lease must be tracked, updated for modifications, and reported under ASC 842. Without automation, the accounting team would spend weeks preparing disclosures. With SOFT4Lessee, they import all contracts, let the system calculate liabilities and ROU assets, and generate a complete ASC 842 statement of cash flows example in minutes.

Ongoing compliance support

ASC 842 compliance is not a one-time task. Leases change frequently — they may be renewed, extended, or terminated early. SOFT4Lessee makes ongoing compliance easier by:

Automatically adjusting schedules for modifications

Keeping all lease contracts in one central repository

Providing built-in disclosure templates that are always audit-ready

By automating compliance and reporting, SOFT4Lessee reduces risk, saves time, and ensures accuracy in every reporting cycle.

Frequently asked questions about ASC 842 cash flow presentation

How are lease payments presented on the cash flow statement under ASC 842?

Finance lease principal payments are deposited into financing activities, while finance lease interest payments and operating lease payments are presented in operating activities.

What is the difference between operating and finance lease cash flow classification?

Operating leases are straightforward - the entire payment goes to operating activities. Finance leases require a split between principal (financing) and interest (operating).

What are the key disclosure requirements for ASC 842 cash flows?

Organizations must disclose total cash paid for leases, broken down by classification. This ensures transparency about lease-related outflows.

How does SOFT4Lessee support ASC 842 cash flow reporting?

It automates the classification, generates compliance-ready reports, and creates audit trails for every calculation.

Can SOFT4Lessee handle ASC 842, IFRS 16, and AASB 16?

Yes. It is designed to generate parallel reports for multiple accounting standards, which is essential for multinational organizations.

Comparing ASC 842, IFRS 16, and AASB 16 cash flow requirements

Lease accounting is not uniform across the world. While the United States follows ASC 842, many international businesses must also comply with IFRS 16 (International Financial Reporting Standards) or AASB 16 (Australian Accounting Standards Board). At first glance, these standards look similar, all aim to bring leases onto the balance sheet, but they differ in how lease payments are treated in the statement of cash flows. Understanding these differences is critical for multinational companies, as the same lease may appear differently depending on the standard applied.

ASC 842 (US GAAP)

ASC 842 is designed to improve transparency without completely overhauling the treatment of operating leases in the cash flow statement.

Finance leases:

Principal portion → classified as financing activity

Interest portion → classified as operating activity

Operating leases:

Entire lease payment → classified as operating activity

This approach creates a distinction between finance and operating leases. It preserves comparability with historic US GAAP reporting while still recognizing lease obligations on the balance sheet.

IFRS 16 (International)

IFRS 16 takes a different approach, aiming for a single model of lease accounting. Under IFRS 16, almost all leases are treated similarly to finance leases under ASC 842.

Lease liability payments:

Principal portion → classified as financing activity

Interest portion → classified as either financing activity or operating activity, depending on accounting policy choice

This means that under IFRS 16, operating leases no longer appear fully in operating cash flows. Instead, much of the lease payment shifts to financing activities, which can make operating cash flow look stronger compared to ASC 842.

For example, a company with large property leases may report lower operating cash outflows under IFRS 16 than it would under ASC 842. This difference can affect key ratios such as operating cash flow coverage and free cash flow, making cross-border comparisons tricky.

AASB 16 (Australia)

AASB 16 is Australia’s equivalent of IFRS 16, adopted by the Australian Accounting Standards Board. In practice, it mirrors IFRS 16, with only minor adjustments for local reporting rules.

Lease liability payments:

Principal portion → classified as financing activity

Interest portion → classified as either financing or operating, based on policy choice

Operating leases:

Like IFRS 16, treated in the same way as finance leases, removing the operating lease category from cash flow classification

For Australian companies, the main difference lies in additional disclosure requirements specific to AASB. However, in terms of cash flow presentation, AASB 16 aligns with IFRS 16.

Best practices for lease data preparation and transition to ASC 842

Transitioning from ASC 840 to ASC 842 requires more than just learning new rules. Success depends on preparing accurate, complete lease data. Poor-quality data is one of the biggest challenges organizations face.

Best practices include:

Collect all lease contracts: Many businesses underestimate their lease portfolios. Be thorough — include real estate, vehicles, and even office equipment.

Abstract key terms: Capture start dates, end dates, payment schedules, renewal options, and escalation clauses.

Clean data: Resolve inconsistencies, remove duplicates, and ensure contracts are complete.

Use software tools: Automate calculations and reporting with systems like SOFT4Lessee to avoid manual errors.

Maintain documentation: Keep audit trails for all contracts and adjustments.

Organizations can reduce risk and ensure a smooth transition to ASC 842 by following these steps.

Get started with SOFT4Lessee for ASC 842 lease accounting

Managing leases under ASC 842 doesn’t need to be overwhelming. SOFT4Lessee helps organizations of all sizes comply with the standard efficiently.

For example, a mid-sized company with 200 leases once spent weeks preparing disclosures. After adopting SOFT4Lessee, it could produce an accurate ASC 842 cash flow statement presentation in hours. Audits became smoother, and management gained more confidence in the numbers.

The software scales for small and large portfolios. Smaller firms can start with an Excel-based calculator, while larger organizations can use enterprise licenses that handle thousands of leases. Each client receives training resources and a dedicated partner manager for support.

By adopting SOFT4Lessee, companies gain accurate reporting, faster close cycles, and reduced compliance risk.

Ensuring accurate ASC 842 cash flow reporting with automation

ASC 842 has transformed how leases are reported. Companies must now recognize right-of-use assets and lease liabilities and carefully classify payments in the statement of cash flows. While this improves transparency, it also adds complexity.

Using an ASC 842 cash flow statement example helps illustrate the changes, but software like SOFT4Lessee makes compliance manageable. SOFT4Lessee helps organizations stay compliant and reduce the burden of lease accounting by automating calculations, supporting multiple standards, and providing audit-ready reports.

For companies preparing for the next reporting cycle, investing in automation is no longer optional - it’s a practical step toward accuracy, efficiency, and long-term compliance.